The global financial landscape has shifted. We are no longer living in an era defined by simple savings accounts and periodic stock market check-ins. In 2026, the velocity of capital, the integration of artificial intelligence into personal banking, and the democratization of complex investment vehicles have fundamentally rewritten the rules of wealth accumulation. To thrive today, one must move beyond the basic “earn more than you spend” mantra and adopt a sophisticated, tech-forward approach to fiscal management.

I. The Algorithmic Transformation of Personal Finance

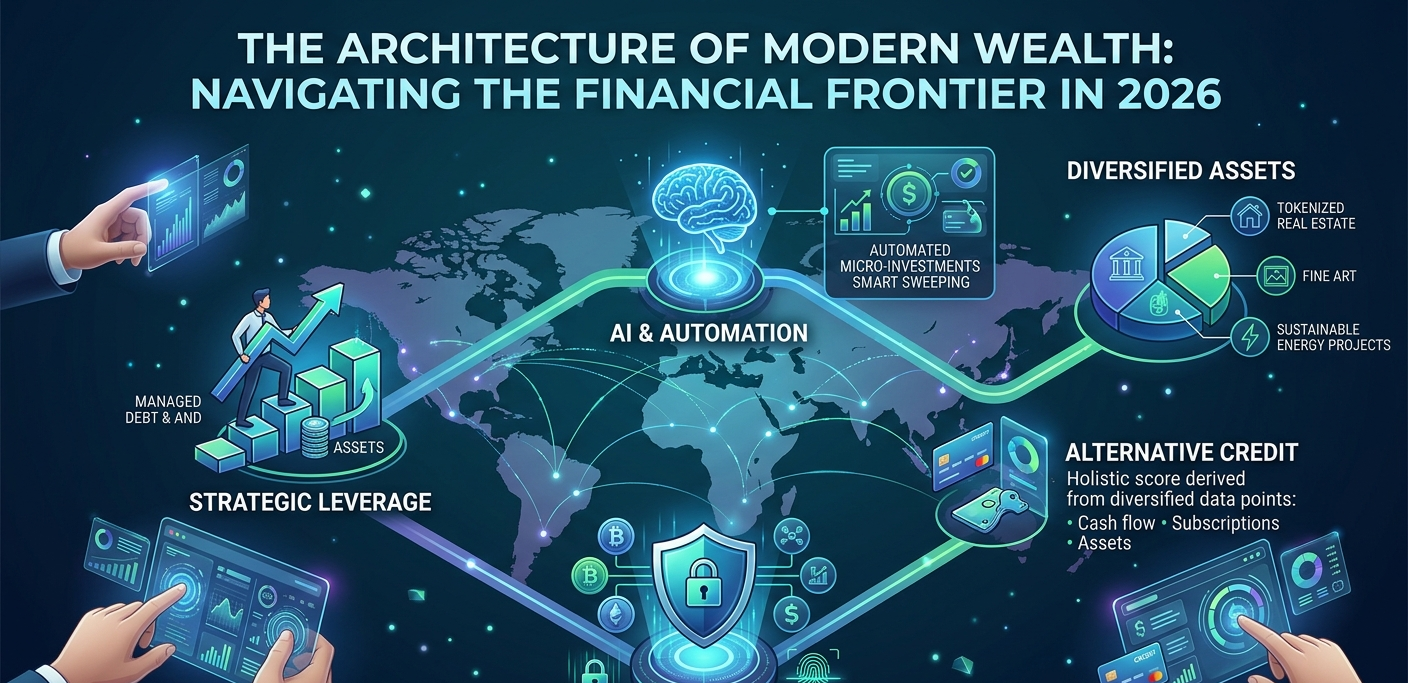

The most significant change in the last five years is the shift from reactive to predictive finance. Previously, a consumer would check their bank balance to see what they had spent. Today, the focus is on what they will spend.

The Death of the Spreadsheet

For decades, the spreadsheet was the gold standard for the financially disciplined. However, manual data entry is prone to human error and latency. In 2026, Autonomous Finance has taken center stage. This involves AI-driven systems that sit atop your bank accounts, analyzing every transaction in real-time. These systems don’t just categorize your spending; they predict your cash flow for the next 90 days with startling accuracy.

Smart Sweeping and Micro-Optimization

One of the most powerful tools in the modern arsenal is “Smart Sweeping.” By analyzing your volatility—the gap between your highest and lowest balance points—AI can identify “lazy capital.” This is money sitting in a zero-interest checking account that isn’t needed for upcoming bills. The system automatically “sweeps” this capital into high-yield environments, such as overnight money market funds or automated micro-investments, ensuring that every dollar is earning a return every single second.

II. The Evolution of Assets: Beyond the Traditional Portfolio

The 60/40 portfolio (60% stocks, 40% bonds) was the bedrock of 20th-century investing. In 2026, that model is considered antiquated. Modern diversification requires a broader lens that includes digital assets, fractional ownership, and ESG-centric (Environmental, Social, and Governance) allocations.

1. The Institutionalization of Digital Assets

Digital currencies and blockchain-based assets have moved from the fringes of “speculative gambling” to a legitimate asset class. Most major brokerage firms now offer direct integration of digital wallets. The key in 2026 is utility-based investing. Investors are no longer just buying “coins”; they are investing in the underlying protocols that power global supply chains, decentralized identity, and cross-border payments.

2. Fractional Ownership: The Great Equalizer

Perhaps the most democratic shift in finance has been the rise of fractionalization. In the past, owning a piece of a high-rise in Manhattan or a rare masterpiece by a world-renowned artist required millions of dollars. Today, through tokenization, an individual can invest $500 into a diversified portfolio of commercial real estate or fine art. This allows for institutional-grade diversification for the retail investor, reducing the overall risk profile of a personal portfolio.

3. The Green Premium

Sustainability is no longer just an ethical choice; it is a financial imperative. As global regulations tighten around carbon emissions, companies with high “Green Alpha”—the ability to generate returns through sustainable practices—are outperforming their peers. In 2026, a “future-proof” portfolio must account for climate risk, as legacy industries face the threat of stranded assets.

III. Credit, Debt, and the New Identity

How we prove our “trustworthiness” to lenders has undergone a radical overhaul. The traditional credit score, while still relevant, is being augmented by a much broader set of data points known as Alternative Credit Scoring.

The Holistic Financial Profile

Lenders in 2026 are increasingly looking at your “Digital Financial Footprint.” This includes:

- Cash Flow Consistency: Are you consistently bringing in more than you spend, regardless of your employer?

- Subscription Reliability: Do you maintain your recurring obligations (SaaS, utilities, streaming) without default?

- Asset-Backed Credibility: Instead of just looking at debt, lenders are looking at your liquid and semi-liquid digital assets as collateral.

Strategic Debt Management

Debt is no longer viewed as a binary “good” or “bad.” In a landscape where inflation can fluctuate and interest rates are dynamic, Strategic Leverage is a key skill. High-net-worth individuals and savvy digital entrepreneurs use low-interest margin loans against their investment portfolios to fund lifestyle needs or business expansion, avoiding the “tax hit” that would come from selling assets.

IV. The Creator Economy and the New Revenue Streams

The traditional 9-to-5 income model is being supplemented—and in many cases replaced—by the “Poly-Income” model. The rise of digital platforms has allowed individuals to monetize expertise, attention, and niche skills on a global scale.

Monetizing Intellectual Property

In 2026, your most valuable asset might not be your house, but your digital IP. Whether it’s a high-traffic niche website, a specialized newsletter, or a series of automated digital products, these assets provide “Scalable Income.” Unlike a salary, which is tied to time, digital IP generates revenue 24/7 with minimal marginal cost.

The Importance of Platform Diversification

For those earning in the digital space, “Platform Risk” is the new market volatility. Relying on a single algorithm or ad network is a recipe for disaster. Successful finance in 2026 involves diversifying your traffic and revenue sources—mixing direct-to-consumer subscriptions with affiliate marketing, sponsored content, and automated ad placements.

V. Security in a Borderless World

As our wealth becomes increasingly digital and decentralized, the threats to that wealth have evolved from physical theft to sophisticated cyber-adversaries.

The Multi-Vault Strategy

Professional financial security now requires a “layered” approach:

- The Transactional Layer: A standard bank account for daily expenses, protected by biometric multi-factor authentication.

- The Growth Layer: Standard brokerage accounts with institutional-grade security.

- The Cold Layer: For long-term digital holdings, “Air-Gapped” cold storage—where the private keys never touch the internet—is the only way to ensure 100% protection against hacking.

Guarding Against “Deepfake” Fraud

One of the emerging challenges of 2026 is the use of AI to mimic voices and faces for fraudulent bank transfers. Financial literacy now includes Digital Sovereignty: learning how to use encrypted communication channels and hardware-based security keys to authorize significant movements of capital.

VI. Tax Optimization in the Digital Age

Tax laws are struggling to keep up with the pace of technological change, but the core principles of optimization remain the same: Locate, Timing, and Structure.

- Location: For digital nomads and global entrepreneurs, where you are tax-resident is a strategic decision. 2026 has seen a rise in “E-Residency” programs that allow for more flexible tax planning.

- Structure: Utilizing corporate entities to hold digital assets can provide significant tax deferral opportunities, allowing capital to compound more efficiently over time.

- Automated Tax-Loss Harvesting: AI tools now monitor portfolios daily to sell losing positions and immediately buy similar (but not identical) assets, locking in tax deductions to offset future gains without changing the portfolio’s risk profile.

VII. The Psychology of Wealth: Staying Grounded in a High-Speed World

Perhaps the most overlooked aspect of finance in 2026 is the mental toll of a 24/7 market. When your net worth is updated every second on your wrist or phone, it is easy to fall prey to “Ticker Shock”—the emotional volatility caused by watching minor market fluctuations.

The “Set and Forget” Philosophy

Paradoxically, the best way to handle high-speed finance is to slow down. The most successful investors in 2026 are those who use technology to automate the mechanics of their finance but remain disciplined in their strategy. They set their parameters—their risk tolerance, their long-term goals, their automated contributions—and then they step back.

Wealth as a Tool for Sovereignty

Ultimately, the goal of modern finance isn’t just a higher number in a digital wallet. It is Sovereignty. In a world of shifting job markets and rapid technological disruption, financial independence is the only true form of job security. It provides the “Freedom Fund” necessary to pivot careers, move across the world, or take a sabbatical to learn a new skill.

Summary: The Five Pillars of 2026 Finance

| Pillar | Focus | Key Tool |

| Automation | Transitioning from manual to autonomous tracking. | AI-Driven Cash Flow Apps |

| Diversification | Including fractional and digital assets. | Tokenized Real Estate Platforms |

| Leverage | Using debt as a strategic tool, not a burden. | Asset-Backed Lines of Credit |

| Sovereignty | Building income streams independent of a single employer. | Niche Digital Assets (Websites, IP) |

| Security | Protecting wealth from digital threats. | Hardware Keys & Cold Storage |

Export to Sheets

Conclusion: Embracing the Horizon

The financial world of 2026 is complex, fast, and occasionally intimidating. However, for those willing to embrace the tools of the era, it offers unprecedented opportunities for wealth creation. We have moved from a world where “high finance” was a gated community to a world where anyone with a smartphone and a strategic mindset can build a global investment portfolio.

The secret to navigating this horizon is a combination of technological literacy and classical discipline. Use the AI to sweep your pennies, use the blockchain to secure your assets, and use fractional platforms to own the world—but never forget that the ultimate goal of money is to provide the freedom to live life on your own terms.

No responses yet